now loading...

The past year has seen a spike in global investors’ interest in Chinese assets. But as the world welcomes the new year, especially after the US presidential election, investors are keen to know what to expect of the China market.

Technology will continue to be a core battleground in 2021, says Aidan Yao, senior emerging Asia economist at AXA Investment Managers. With the change of administration in the United States, the market may expect less US sanctions and technology restrictions against China, but the underlying competition between the world’s two largest economies will remain.

“Overall, there will be some technical changes, but the fundamentals will not change,” Yao says, although he thinks policymaking will become more predictable.

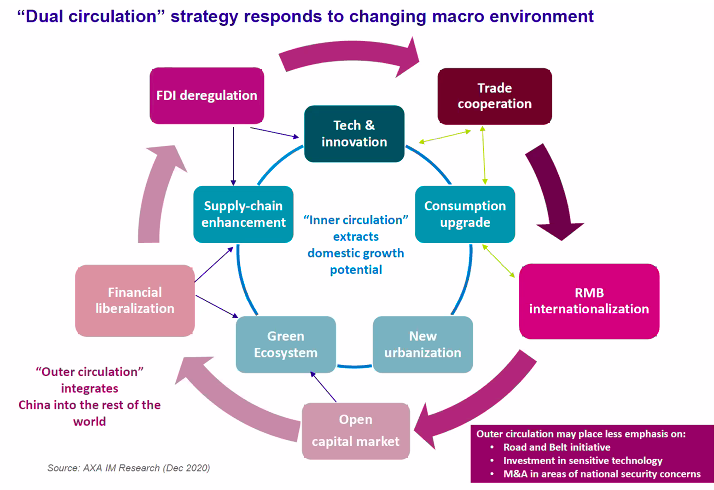

Against this backdrop, China is expected to continue its dual circulation story. Yao explains that Beijing will have four major objectives, namely self-sufficient inner circulation, self-sufficient sustaining economic growth, sustainability and outer circulation.

These objectives will rely on an upgrade of its internal economic growth model and further opening up of its financial markets. “A combination of the opening up of the world’s second largest capital market and making the domestic economy more sustainable by providing a solid backdrop for renminbi assets makes China a very attractive place to park your savings for global investors,” Yao says.

On the equity side, the A-share market is expected to continue attracting global investors. “Enhanced research coverage from global investment banks of the A-share market is also providing more confidence to foreign investors,” says Simon Weston, senior portfolio manager, Asian equity, at AXA Investment Managers.

Sectors relating to the new economy, healthcare and renewable energy offer investment opportunities, according to Weston. The financial technology segment, which of late has been the subject of regulatory scrutiny, particularly with regard to the monopoly-type behaviour of some internet majors, is expected to turn positive in the long term.

On the fixed-income side, Chinese property is an area worth watching. “We remain comfortable with China property,” says Jim Veneau, head of Asian fixed income at AXA Investment Managers.

“We remain positive and constructive [towards the China property sector] through valuation and from fundamentals,” Veneau says. “The sector is known as a high-yield sector but there are a large number of investment-grade Chinese property developers which issue bonds in the offshore market,” he adds.

Strong momentum

Yao predicts that the momentum of renminbi assets will remain strong in the near term. But whether this trend will be sustained in the second half of 2021 is subject to discussion.

“If you look at the quarter-on-quarter projection for this year, we expect the economic growth [of China] to be fairly strong, but essentially level off in the second half of this year. This is primarily because of the reduction of fiscal and monetary stimulus measures,” Yao says, noting that renminbi assets are likely to be less attractive.

Explaining the strength of the renminbi in 2020, he notes: “China’s trade surplus reached a high rate, which partly was because China was the only factory that opened during the pandemic. So the current account inflows through trade channels were very strong.

“In terms of the capital account, this has to do with the recovered inflows to both onshore equity and bonds. And the onshore bonds were boosted by the widening interest rate differentials – China’s interest rate has already gone back to pre-Covid levels whereas that of the US and Europe has been nailed to the ground,” Yao says.

But he notes that as the rest of the world starts to recover, China would no longer be the only factory opened. The US economy will recover with help of vaccines, meaning the trade surplus and interest rate differential between China and the US should gradually narrow, and this will ultimately reduce the attractiveness of renminbi assets.