now loading...

I’m taking a break from Europe’s geopolitical struggles to tackle something altogether different, but something that is almost guaranteed to get consumers exercised: car parking. My trigger was the sinking into administration of National Car Parks ( NCP ), the UK car park operator and a former icon in its field.

It seems almost counter-intuitive that a company offering car parking in clogged towns and cities might face insolvency. After all, private parking operators are everywhere, while multi-year efforts to get us out of our private vehicles into mass transportation as a core component of sustainable living have clearly not worked as intended.

So what happened to NCP? Its Japanese owner, Park24, and administrators PwC, separately note that NCP’s performance deteriorated post-Covid as demand for parking failed to recover to historic levels. “Continued shifts in commuting and customer driving patterns have impacted site occupancy,” PwC notes,” while the high concentration of long-term, inflexible leases has meant NCP has been unable to reduce costs in line with revenue or to exit loss-making sites, resulting in ongoing trading losses.”

Park24 made NCP’s financial position crystal clear, citing liabilities of £352.64 million ( US$467.5 million ) and assets of £53.23 million and noting that persistently high inflation in the UK had led to rising inflation‑linked rent payment obligations while new car park developments to support revenue growth and cost‑reduction measures had failed to counterbalance the slow recovery in demand, leading to continued structural losses.

With significant rent payments falling due at the end of March 2026, Park24 said NCP’s cash‑flow position had tightened and it had become increasingly difficult to secure the necessary funding. NCP, ultimately, had insufficient cash to meet its financial obligations.

Serial value extraction

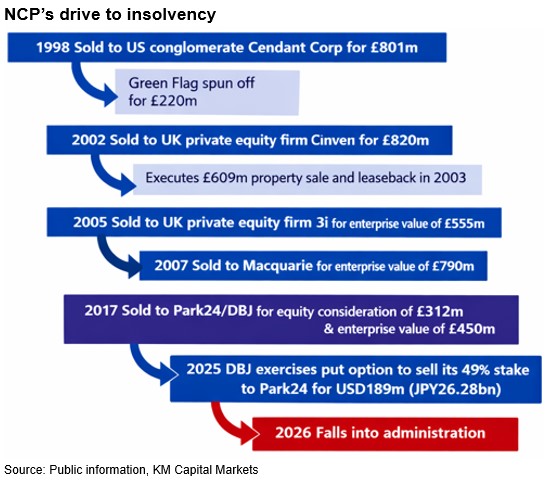

Slow post‑Covid recovery may have been the trigger, but more than two decades of ownership churn will have left NCP structurally more brittle. The company has been around since 1931 but like other operators in the field, it had been tossed around as financial buyer after financial buyer sucked out value and passed it on.

When fabled British entrepreneurs Ronald Hobson and Donald Gosling sold NCP to highly acquisitive US conglomerate Cendant Corp in 1998, they had owned the business for almost 40 years, having acquired it in 1959 from the original 1931 founder Frederick Lucas to build out their business of developing car parks on bomb sites in the UK after World War II.

Including the sale to Cendant, NCP went through five sales processes by the time it filed for administration. Across five ownership cycles, NCP was repeatedly reshaped to suit the priorities of successive acquirors, often with an emphasis on extracting value early rather than building long‑term resilience.

When NCP ran out of road, it was Park24, the Japanese parking, car rental and car sharing services company, that was left holding the wreckage rather than a financial sponsor. Its 2017 acquisition of NCP, in partnership with Japanese government agency Development Bank of Japan, was its big expansion play. Outside of Japan, Park24 had operations in Singapore, Malaysia, South Korea, Taiwan, Australia and New Zealand. NCP was its big move into Europe.

Park24’s final big corporate action before filing for administration was in November 2025, a dubious privilege as it involved acquiring DBJ’s 49% stake for 29.28 billion yen ( US$189 million ) to become sole shareholder in a business it likely knew was terminal. DBJ had held a put option on its NCP stake as part of the shareholders’ agreement.

Circling for opportunities

Despite NCP’s terminal decline, parking in the UK remains a highly competitive but highly fragmented business. Rivals – and there are many – will be closely circling NCP’s portfolio of 340 facilities as PwC prepares a sale. It’s hard to judge whether and to what extent any of NCP’s sector rivals are experiencing the same business pressures.

The working-from-home phenomenon is still very much in evidence, the rise and rise of e-commerce continues to pressure retail footfall, while the cost-of-living crisis that kicked off with Russia’s invasion of Ukraine is about to be extended by the global economic fallout from war in the Middle East. NCP’s business model is unlikely to have been unique, but the degree of buzz in mergers and acquisitions and buyouts in and around the parking and mobility sectors suggests the insolvency will not have derailed the excitement at emerging sector opportunities.

In a report from JLL, the commercial real estate services and investment management company ( ‘All change for car parks?’ ), Colin Chan, Head of Car Park Solutions & Investments said this: "We foresee a transformation in the car park sector characterized by innovative new designs, forward-thinking repurposing, initiatives driven by sustainability and optimization powered by data. An increasingly vital aspect is the seamless integration with new mobility services alongside mass adoption of electric vehicles. The demand for efficient parking solutions is set to only increase, making the car park sector a promising realm for investment”.

The chart below shows a healthy level of investment in the parking sector in the UK, which has developed a truly international profile.

Aggressive digitalization

Managing car parks has long ceased being about managing multi-story slabs of concrete. The parking sector has been vertically integrated and aggressively digitalized, turning what were once stand‑alone buildings into nodes in a much larger data ecosystem. Automatic number plate recognition ( ANPR ) cameras, CCTV, digital payments, digital pre‑booking platforms, location‑based services and back‑end analytics now sit behind almost every barrier and pay station.

UK operators aren’t just managing bays; they’re running real‑time traffic, pricing and enforcement systems that plug into payment processors, mapping apps, Driver and Vehicle Licencing Agency government data feeds and outsourced compliance engines.

This transformation hasn’t happened in a vacuum either: local authorities too have been on their own parallel technology drive, deploying increasingly sophisticated digital systems to manage road space and traffic flow. High‑definition cameras, sensor‑driven traffic signals, real‑time congestion monitoring and network‑wide data platforms now underpin everything from bus‑lane enforcement to low‑traffic neighbourhoods.

Parking digitalization is just one strand of a broader shift in which the UK mobility network is being instrumented and monetized through technology.

Public hostility

Monetisation in this arena has become a hot-button topic, because layered onto all of the opportunities for operators to generate steady revenues schemes is a growing sense of frustration among motorists that parking and motoring technology is being used less to manage and streamline mobility and more to maximise revenue at users’ expense.

Drivers have a lot to moan about: the appalling state of British roads, traffic overload, a lack of electric vehicle charging points, and road schemes designed to create traffic bottlenecks. In London – average driving speed 10.3 miles per hour – there’s the congestion zone that digitally charges drivers £18 to £21 per day to drive close to or into central London, ultra-low emission zones ( ULEZs ) that force drivers to pay £12.50 per day if their vehicles aren’t ULEZ compliant, 20 miles per hour speed limits on half the roads and giving precedence on roads to bicycle users. And the end of all of that, drivers are confronted by what they see as exorbitant parking charges.

UK local authorities face persistent allegations of installing technology principally in money‑generating entrapment schemes through poorly located, confusing or effectively invisible road signage, or entrapment schemes dressed up as anti-pollution low traffic neighbourhoods. Both have triggered record number of high-priced digital penalty notices.

Private parking companies attract similar if not worse criticism. The contractual terms drivers are deemed to have accepted when they drive into car parks located on private land often hinge on signage that is hard to find, hard to read or deliberately ambiguous, while ANPR‑driven enforcement and aggressive invoicing have pushed the volume of private parking charges to record highs. Predatory payment enforcement tactics make consumers feel vulnerable.

The result is a widespread perception that the digitalization of parking and road management has tilted the playing field decisively against consumers. In that light, NCP’s administration becomes not so much a story about a failing operator but more a reminder of the strange dissonance at the heart of the sector: a business model that provokes deep public resentment even as its underlying assets and technology continue to attract intense corporate interest.